What are Exchange Traded Notes (ETNs)?

Introduction

Exchange Traded Notes (ETNs) are senior unsecured debt securities that are typically issued by a bank. ETNs are a type of “structured product,” and have a return that is based upon the performance of an underlying index or other underlying asset, such as a basket of stocks.

We have prepared this document to help explain ETNs to investors, and to describe their key terms. We will also compare some features of ETNs to other products, particularly Exchange Traded Funds (ETFs), which are products that may be more familiar to some investors. We also will describe some of the key risks relating to ETNs.

Key Terms of ETNs

Structure: ETNs are the issuer’s senior unsecured debt securities. They are not backed by any specific assets. For example, if an ETN is linked to a stock index, the issuer will not own a pool of the relevant stocks for the benefit of ETN owners. Accordingly, ETNs are subject to the issuer’s credit risk, and changes in the issuer’s credit ratings may affect their market value.

Underlying Asset: Unlike most traditional debt instruments, ETNs do not pay a conventional fixed or floating rate of interest, followed by the repayment of principal at maturity. Instead, the payments on the ETNs are linked to the value of an underlying index or other asset, such as a basket of stocks. Different ETNs are linked to many types of underlying assets, ranging from large-cap to small-cap stocks, U.S. and non-U.S. securities, commodities and currencies. As the value of the relevant underlying asset increases or decreases, so too does the value of the ETN. The payment at maturity (or upon an earlier call or redemption) can be significantly greater than or less than the principal amount.

Payment Formula: The specific payout on an ETN will be set forth in the applicable offering documents. Investors should carefully review that formula to determine if it is consistent with their investment objectives. For example, an ETN may provide a payout that increases or decreases on a one-to-one basis with changes in the underlying asset (subject to fees), or a payout that involves leverage or other different return.

Interest: Most ETNs do not pay interest. However, some ETNs pay a “conditional coupon” that, for example, may be based on the dividend rate of the securities that comprise an underlying index.

Listing: ETNs are listed on a securities exchange and can be bought and sold at market prices during the trading day.

Leverage: ETNs can offer investors terms that include leverage or inverse leverage that resets periodically. Some of the most popular versions of leveraged and inverse leveraged ETNs include daily resetting leverage. That is, investors receive the daily return of the underlying index multiplied by the specified leverage amount. Leveraged and inverse leveraged ETNs involve additional risks. For example, these leveraged, inverse and inverse leveraged ETNs typically seek a return on the underlying index for only a single trading day. Those leveraged and inverse leveraged ETNs are not “buy and hold” investments, and should not be expected to provide the indicated return of the underlying index’s cumulative return for periods greater than a day.

Management: An ETN does not hold or invest in any assets.

Instead, its payments are linked mathematically to the performance of the underlying index or other asset. Accordingly, an ETN does not have any investment manager or investment advisor.

Fees: ETNs involve fees that impact an investor’s returns. Typically, for ETNs that seek to replicate an index, an investor fee will reduce the potential return on the ETNs. In addition, for leveraged and inverse leveraged ETNs, an additional financing fee or similar fee will reduce the potential return on the ETNs. An ETN’s fees will be set forth in the relevant offering documents.

Principal Differences from ETFs

Structure: An ETF is organized as a separate entity. This entity holds the relevant assets that it tracks.

Management: An ETF will have an investment advisor, that makes purchase and sale decisions as to its investments, based upon the strategy set forth in the ETF’s offering documents.

Fees: An ETF will involve fees that result from its structure and operations. For example, a portion of an ETF’s assets will be used to pay the fees relating to its organization and its ongoing management, and commissions relating to its ongoing purchase and sale of the relevant assets. These fees will reduce the potential returns on the ETFs.

Tracking Error: Tracking error is the annualized standard deviation of daily return differences between the total return performance of an ETF or an ETN, on the one hand, and the total return performance of the underlying index on the other hand. An ETF’s or ETN’s total expense ratio is often used as an indicator of future tracking difference. For example, if an ETF charges 1% to track an index, then ETF returns should lag the index returns by 1%. As noted above, both ETFs and ETNs charge fees and expenses that are not applicable to the relevant underlying index or asset, but do impact the returns realized by investors. ETNs provide investors with the ability to gain exposure to an underlying index or asset with only minor tracking error, arising from the fees included in their terms.

For ETFs, on the other hand, a more significant tracking error can exist between the returns of many ETFs and their underlying indices or assets. A few reasons why the more significant tracking error exists with ETFs are:

- Transaction and Rebalancing Costs: The net asset value of an ETF will reflect transaction and rebalancing costs and fees, such as when securities or other underlying assets are purchased and sold; these costs and fees are not applicable to an underlying index. When an ETF is tracking an index with many securities or illiquid securities, or an index that rebalances frequently by design (such as an equal-weighted index), the ETF will incur greater transaction and rebalancing costs, which will increase the tracking difference;

- Sampling: To save on costs, an ETF may not invest in all the securities, futures contracts or commodities comprising its underlying index, but instead, may invest in, for example, a “representative sample” of those assets. This sampling may result in an increased tracking difference for ETFs;

- Timing: When an index rebalances or reconstitutes its components, the changes are instantaneous, based on the index methodology. In contrast, an ETF tracking an index must realign itself with the index, and may not fully replicate the performance of its underlying index due to the temporary unavailability of certain securities, futures contracts or commodities comprising the underlying index. During the time it takes an ETF manager to buy and sell the necessary securities, securities prices may change, creating tracking difference between the index and the ETF;

- Cash Drag: Some ETFs receive dividend distributions from their underlying securities and distribute them to ETF shareholders. However, ETFs do not distribute these dividends on a real-time basis; instead, they do so periodically. As a result, an ETF may maintain a certain portion of its portfolio in cash or cash equivalents, which may be temporarily reinvested, which results in transaction costs. The cash drag will result in an ETF having slightly different returns than the fully invested index, causing tracking difference.

For ETNs, most of these factors are not applicable. The terms of an ETN promise to the holder a return that is mathematically linked to the return of the underlying index or assets, minus fees.

Diversification: Most ETFs are registered as open-end investment companies (i.e., mutual funds); like mutual funds, they are required by federal tax laws to be diversified. Generally speaking, with respect to one half of the fund’s assets, no more than 5% may be invested in the securities of any one issuer; with respect to the other half, no more than 25% may be invested in the securities of any one issuer. In other words, the minimum diversification a fund could have is 25% of its assets in each of two issuers, and 5% of its assets in each of 10 additional issuers. In addition, if a fund elects to be diversified for purposes of the Investment Company Act (and most do), the requirements are even more stringent than under the tax laws—with respect to 75% of its portfolio, no more than 5% may be invested in any one issuer. Therefore, a majority of ETFs are invested in a minimum of 20 issuers.

ETNs, on the other hand, due to their structure as a debt instrument, are not subject to the same diversification requirement. Instead, ETNs may track equity indexes or baskets with as few as 10 issuers. This allows investors to obtain concentrated “micro” sector exposure.

Tax Treatment and Tax Efficiency: Although the income tax treatment of ETNs can be subject to uncertainty, ETNs are typically treated as prepaid forward contracts for U.S. federal income tax purposes.

Under that treatment, an investor in an ETN that does not pay periodic coupons generally will be subject to tax only when it disposes of the ETN (whether in a sale, a redemption or at maturity). So long as an investor holds an ETN for at least a year, the investor will recognize long-term capital gain or loss upon that disposition. However, an investor in an ETN that pays periodic coupons (including conditional coupons) will be subject to current tax on those coupons, generally at ordinary income rates.

By comparison, an investor in an ETF usually will be subject to tax each year that it holds the ETF. Because ETFs actually hold underlying assets, if an ETF that is taxable as a pass-through entity (most are) sells its assets, or otherwise changes its composition, the ETF holders have to pay any resulting capital gains tax in that year. Additionally, ETFs are required to make yearly income and gain distributions to its investors, which are taxable. A further tax advantage of investing in an ETN is that an ETN is not structured as an entity (such as a corporation or partnership); instead, it is a debt instrument. An ETF, on the other hand, has to be set up as an entity in order to hold the underlying assets. Being formed as an entity can have a number of tax disadvantages. For example, commodity ETFs are typically structured as limited partnerships and hold futures contracts that are taxed annually, regardless of whether the position was bought, liquidated, or simply held. Investors in a commodity ETF will incur taxes simply holding an ETF throughout the year.

ETFs formed to invest in Master Limited Partnerships (MLPs) typically are set up as corporations, which have the disadvantage of being subject to “double taxation.” This means that any income of an MLP ETF will be subject to tax at the entity level, thereby reducing the amount available for distribution to investors (who will then also have to pay tax on the income distributed to them). An ETN tracking those same commodities or MLPs will not have the same disadvantages.

Additional Benefits of ETNs

Ease of Ownership: ETNs are listed on an exchange and can be bought and sold during the trading day. Most ETNs have a market maker that helps to promote their liquidity. A market maker will typically create a two-way market in the ETN, so that when an investor wants to sell the ETN, the market maker will buy it, and vice versa. Access to New Markets, New Strategies: Unlike many ETFs, ETNs can provide, on a cost-effective basis, access to investment strategies that are not easily accessible in many investment products, such as ETNs that offer exposure to commodity and commodity futures, volatility futures, a basket of less than 20 stocks, a basket of stocks concentrated in a single sector, leverage and inverse baskets and replication or strategies with high turnover.

Leverage and Inverse Exposures: Some ETNs promise the return of 200% or 300% of the performance of an index (resetting daily). If the index increases by 1%, then the 200% leveraged ETN would gain 2% and the 300% leveraged ETN would gain 3%, before fees, for that day. Conversely, if the index decreases by 1%, then the 200% leveraged ETN would lose 2% and the 300% leveraged ETN would lose 3%, before fees, for that day.

The inverse is true for ETNs that provide inverse exposure to an index. If the applicable index decreases by 1%, then the -200% inverse leveraged ETN would gain 2% and the -300% inverse leveraged ETN would gain 3%, before fees, for that day. Conversely, if the index increases by 1%, then the -200% inverse leveraged ETN would lose 2% and the -300% inverse leveraged ETN would lose 3%, before fees, for that day.

These ETNs are intended to be daily trading tools for sophisticated investors to manage daily trading risks. They are typically designed to achieve their stated investment objectives on a daily basis.

Replication and Trend-Following Strategies

ETFs have gradually become more advanced, a trend perhaps best evidenced by the introduction of hedge fund replication products. Trend-following strategies are one example. These are investment strategies that, for instance, oscillate exposure between cash and an index of stocks or commodities, or among several asset classes, based on a variety of quantitative/algorithmic momentum factors. However, because these strategies usually require assets to be held for a limited period of time, the after-tax returns can be limited.

Because an ETN is a debt instrument that doesn’t actually hold the underlying assets, investors can avoid incurring short-term capital gains and high turnover costs that pass through to ETF investors as additional fund expenses.

Disadvantages and Risk Factors

All ETNs are subject to risks, which will depend upon a variety of factors relating to the structure and terms. Investors should carefully read the offering documents for any ETN prior to making an investment decision.

Potential Loss of Principal: ETNs do not guarantee any minimum payment at maturity or upon an earlier redemption. Depending upon the performance of the underlying asset, an investor can lose all or a substantial portion of the amount invested in the ETNs.

Credit Risk: Since ETNs are debt instruments, investors are subject to the credit risk of the issuer, and potential default by the issuer. This is the primary difference between an ETF and an ETN: ETFs are mainly subject to market risk (that is, changes in the value of the assets that they hold), while ETNs are subject to both market risk and the credit risk or the risk of default by the issuer.

Call Risk: Unlike ETFs, ETNs are usually subject to the issuer’s ability to call the ETN at any time. The call price is typically based on the then-current value of the underlying asset. This can be particularly detrimental to an investor if the issuer calls an ETN at a time when the investor might suffer a loss.

Issuance and Liquidity Risk: The issuer of an ETN is not required to issue more ETNs to meet investor demand. As a result, the indicative value of an ETN may be substantially different than the price at which an investor can buy or sell the ETN (i.e., a premium or a discount may exist). Additionally, like an ETF, an ETN can be delisted from its exchange under some circumstances. As a result, an investor may be only able to sell an ETN in the over-the-counter market or, and depending on how many ETNs they own, sell the ETNs directly back to the issuer. In both scenarios, there would be a lack of liquidity and performance transparency with respect to the ETN. The liquidity of the market for any ETNs can materially change over their term. There may not be sufficient liquidity to enable an investor to sell the ETNs readily, and an investor may suffer substantial losses and/or sell the ETNs at prices substantially less than their expected value.

Premium Risk: If an investor pays a premium for an ETN over the indicative note value, it could lead to significant losses if the investor sells the ETNs at a time when the premium is no longer present (or if the ETN is trading at a discount), or if the ETNs are called at price that is less than the price the investor paid for the ETNs.

Redemption Risk: Instead of selling the ETNs in the market on an exchange, an investor can redeem the ETNs directly with the issuer. However, an issuer typically requires a minimum number of ETN units (for example, 25,000) to be tendered for a redemption. Due to the minimum number of ETNs and the discretion of the issuer to redeem them, the liquidity of the notes (directly with the issuer) may be limited.

Conflicts of Interest: The issuer of the ETNs and its affiliates may play a variety of roles, and may engage in a variety of transactions that are adverse to an investor’s interest in the ETNs. For example, the issuer and its affiliates may engage in hedging and trading transactions that impact the value of the underlying assets or indices to which the ETNs are linked. The issuer and its affiliates may also engage in business transactions with entities that have securities included in a relevant underlying index. Affiliates of the issuer may also issue research reports that express opinions that are inconsistent with an investment in the ETNs.

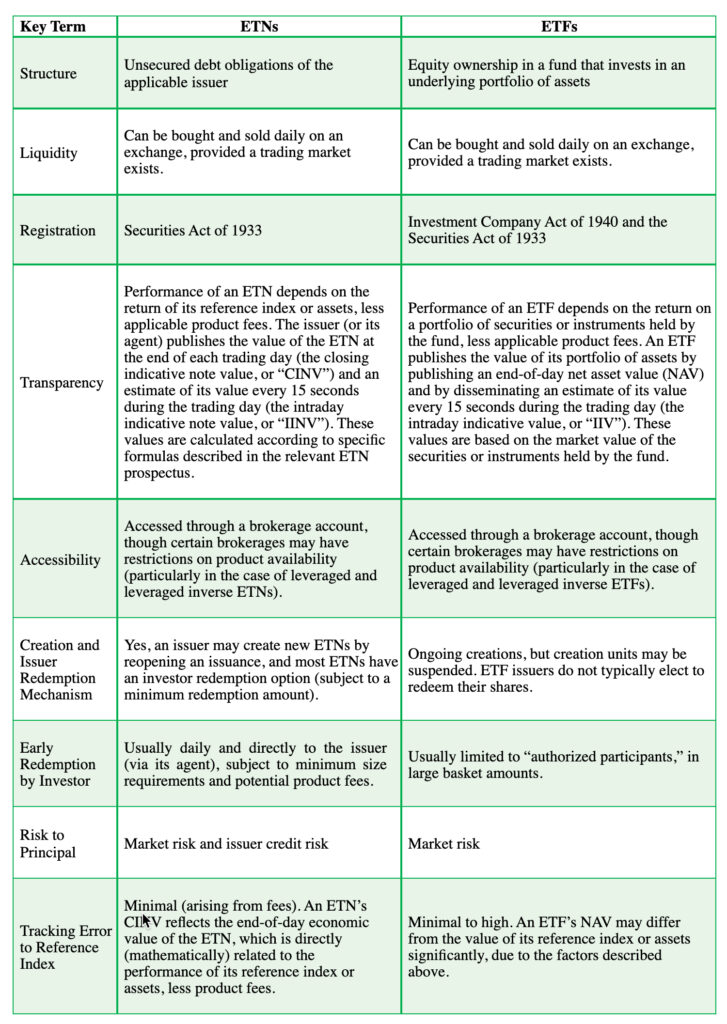

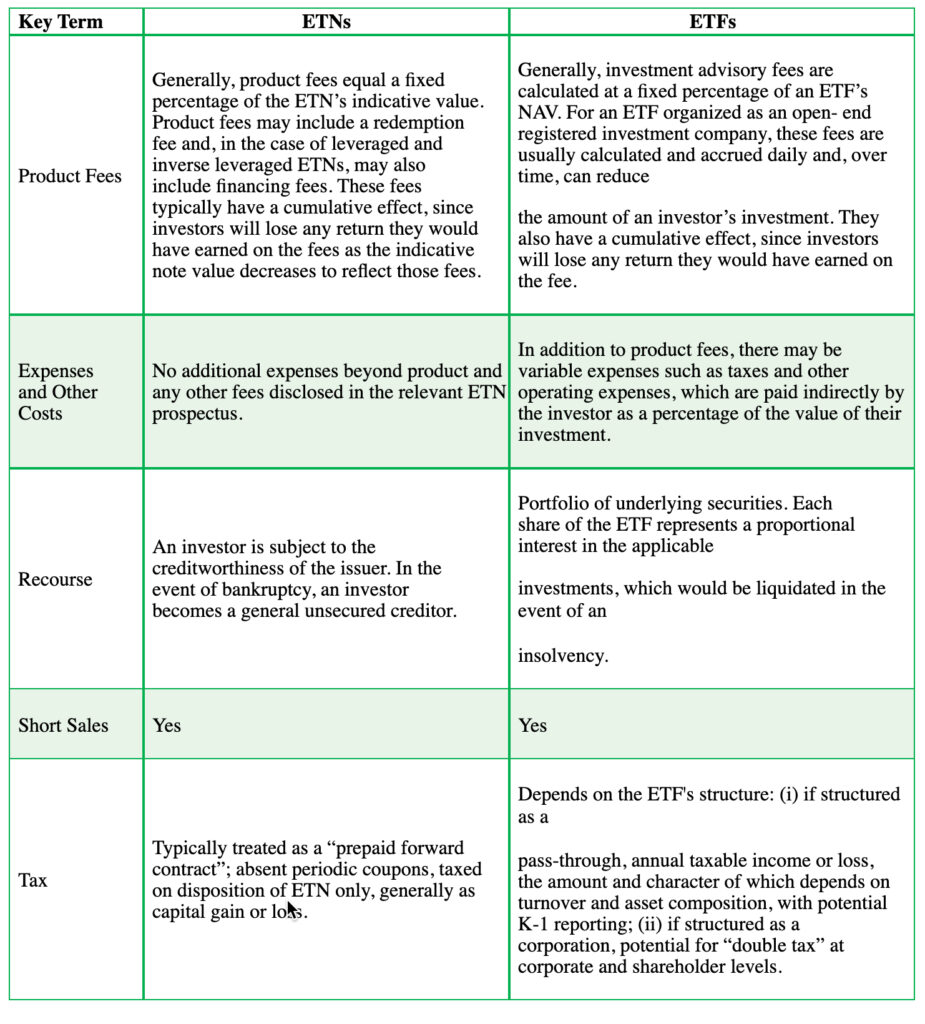

Summary Comparison: ETNs vs ETFs: In order to assist readers in understanding the key similarities and differences between ETNs and ETFs, we have provided the following table:

For further information, please contact:

www.rexshares.com

info@rexshares.com

203-557-6201

Bank of Montreal has filed a registration statement (including a prospectus) with the SEC for the offerings to which this document relates. Before you invest, you should read the prospectus in that registration statement and the other documents that Bank of Montreal has filed with the SEC for more complete information about Bank of Montreal and these offerings. You may obtain these documents free of charge by visiting the SEC’s website at http://www.sec.gov. Alternatively, we will arrange to send to you the prospectus (as supplemented by the applicable supplements) if you request it by calling our agent toll-free at 1-877-369-5412.